With two different taxes (CGST & SGST), five different tax slabs, exclusion of some goods from GST purview & power given to states to set the threshold limit for GST registration in their own, Are we really inch closer towards becoming one nation, one tax, and one market?

Let's understand the today’s scenario.

|

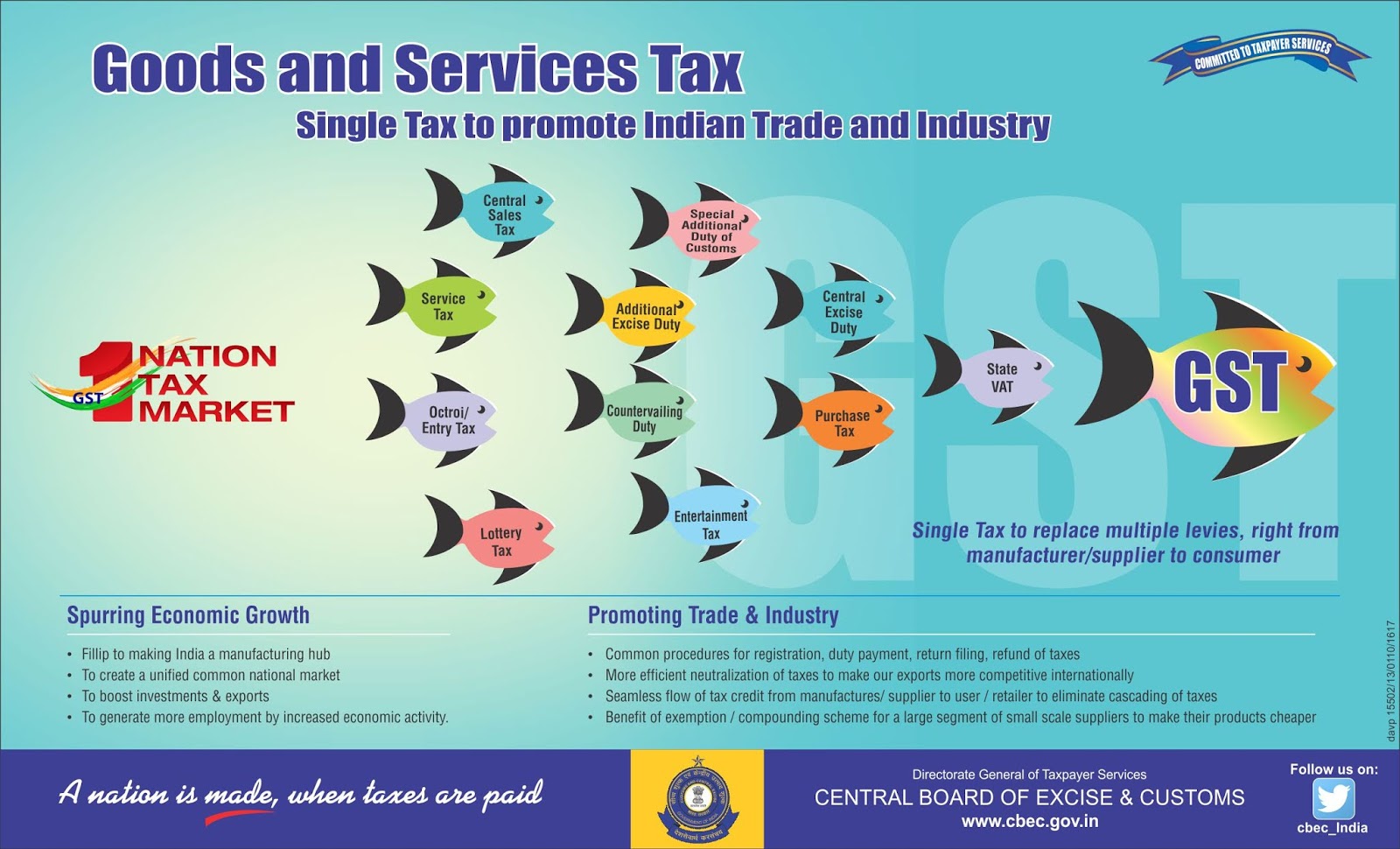

What is GST and how it is one tax, one Market?

- GST is an Indirect Tax which has replaced many Indirect Taxes in India. Goods and Service Tax (GST) is an indirect tax levied on the supply of goods and services. This law has replaced many indirect tax laws that previously existed in India.

- Goods & Services Tax Law in India is a comprehensive, multi-stage, destination-based tax that is levied on every value addition.

- Under the GST regime, the tax is levied at every point of sale. In the case of intra-state sales, Central GST and State GST are charged. Inter-state sales are chargeable to Integrated GST.

- When the Goods and Services Tax (GST) came into force on July 1, 2017, it subsumed almost all host of indirect taxes that were levied (17 previous tax laws)like Central Excise duty, State VAT, Service tax, luxury tax, and others are all gone. So GST law is one indirect tax for the entire country.

One nation, one tax, one market

GST integrated the country into a common market by removing barriers across states and enabling smooth flow of goods from one state to the other. It subsumed various indirect taxes levied by the center and the states to bring in a pan-India uniform indirect taxation system.

Under GST, A seamless flow of credit chain available, so that the tax levied on actual value addition only & effects of cascading (it is the situation where the tax levied on tax) can be neutralized.

In today’s scenario

In an effort to bringing all states on board and to minimize the inflationary impact, India brought in a dual GST with multiple tax rates for both goods and services—fewer slabs would have meant taxing items of common consumption at a higher rate.

Resultant currently GST is divided into five different tax rate slabs:

Sr. No

|

Rate of Tax IGST

|

Rate of Tax CGST

|

Rate SGST

|

1

|

5%

|

2.5%

|

2.5%

|

2

|

12%

|

6%

|

6%

|

3

|

18%

|

9%

|

9%

|

4

|

28%

|

14%

|

14%

|

Further, GST complies the one nation but not one tax systems, there are some products in which the govt. doesn't implement tax like petrol, diesel, power and on alcohol on such product, the govt is taking around 40-50% of tax.

In recent 32nd Council general meeting held in Delhi on 10th of Jan,2019, It has been decided through consensus that The existing threshold limit of Rs. 20 lakhs for obtaining the GST registration and levy of GST has been increased to Rs. 40 lakhs (For states of special importance i.e. north east based states limits increased to Rs. 20 Lakhs).

But the important thing is that the GST Council Meeting has given power to the States to choose the applicable threshold as per their discretion i.e. whether the limit Rs. 20 lakhs or Rs. 40 lakhs. In such a case the state has to communicate their decision council within one week.

This will going to affect the Input credit chain and leads to cascading which is against the dream of one nation, one tax & one market.

With this, we can conclude that, with the introduction of GST we have moved towards the one nation, one tax economy but the truth is with current policy-making and administration, yet we are very far from the dream of one nation, one tax & one market economy.

Author's Note:

For any feedback,

write me at panka.jsa@gmail.com

Author's Note:

For any feedback,

write me at panka.jsa@gmail.com

No comments